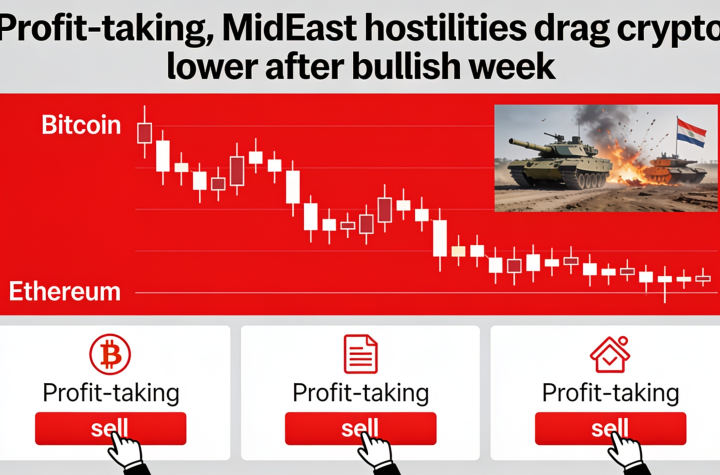

Crypto Market Slides as Profit-Taking and Middle East Tensions Hit Sentiment

Weekend gains in the cryptocurrency market faded into a Monday sell-off as renewed Middle East tensions weighed on investor sentiment, South Korea’s Kospi index plunged 9.2%, and approximately $253 million in leveraged crypto positions were liquidated.

Bitcoin pulled back during Asian and European trading hours on Monday, falling to around $63,100 from above $64,300 at the weekly close at midnight UTC.

The decline represented a drop of roughly 1%, while losses among altcoins were more significant. Lighter (LIT) led the market downturn, falling 8% in its first major correction after surging more than 200% over the previous two months.

Risk aversion extended beyond crypto markets and affected global equities. South Korea’s Kospi suffered a 9.2% decline as SK Hynix, the memory chip company that debuted in U.S. markets on Friday, plunged 15%. Japan’s Nikkei and China’s SSE Composite also dropped more than 2%.

The market weakness came as tensions between the U.S. and Iran intensified, with both sides launching airstrikes amid disputes over control of the Strait of Hormuz.

U.S. stock markets were also expected to open lower, with Nasdaq 100 futures down 0.9% and S&P 500 futures declining 0.25% since midnight.

Despite the pullback, bitcoin and the broader crypto market entered the weekend with strong upward momentum, avoiding immediate downside risks. Monday’s decline may also reflect traders taking profits after the recent rally.

Derivatives Market Overview

Bitcoin derivatives markets remained relatively stable over the past week. Open interest stayed near $17 billion, while the three-month annualized basis remained unchanged at approximately 3.8%.

Funding rates were mostly unchanged and slightly positive across major exchanges, although Bybit stood out with BTC perpetual funding around -13% annualized.

Stable open interest, a steady futures basis, and balanced funding conditions suggest traders are maintaining existing positions without adding significant new leverage in either direction.

Options activity showed a continued bullish bias. The 24-hour put/call ratio favored calls at 64/36, while the one-week delta skew remained elevated at 16%. However, the figure has declined from 26% a week earlier, indicating that demand for call options is slowing rather than accelerating.

The at-the-money volatility curve remains in contango, with short-term implied volatility around 34%-35% and longer-term volatility near 43% through mid-2027, suggesting traders expect relatively stable conditions over the longer term.

According to CoinGlass data, crypto markets recorded $253 million in liquidations over the past 24 hours, with long positions accounting for 76% and shorts representing 24%. Bitcoin led liquidation volume with $70 million, followed by Ethereum at $60 million.

Binance’s liquidation heatmap shows the $62,000 level as an important area to watch if bitcoin faces further downside pressure.

Token Market Highlights

AI-related tokens FET and NEAR showed relative strength, each gaining around 1.5% despite broader market weakness.

Hyperliquid (HYPE) followed Lighter’s decline, dropping about 3.3% to $65.10, its lowest price since July 2.

CoinMarketCap’s “Altcoin Season” indicator reflected the market’s recent volatility, rising to 56/100 from last week’s average of 50. The reading suggests improving risk appetite among investors after months of significant losses.

Cardano (ADA) remained one of the more volatile major tokens. After suffering a 39% decline in June, ADA rebounded more than 40% in early July before giving back part of those gains, falling 19% since July 4.

Solana-based decentralized exchange Jupiter (JUP) also faced pressure, declining more than 15% over the past week as daily trading volume dropped to around $17 million, compared with levels that frequently exceeded $500 million in 2025.

More Stories

AI Chips and Bitcoin: How Transformative Trends Can Still Trigger Massive Market Corrections

Crypto Week Ahead: Inflation Data, Earnings Season and Bitcoin’s Next Move

Bitcoin Dips Under $63K as Korea Stocks Crash, Global Markets Brace for Volatility