Bitcoin’s implied volatility remains subdued even as prices slide and macro pressures build, creating what some options traders see as an attractive setup for volatility strategies such as long straddles.

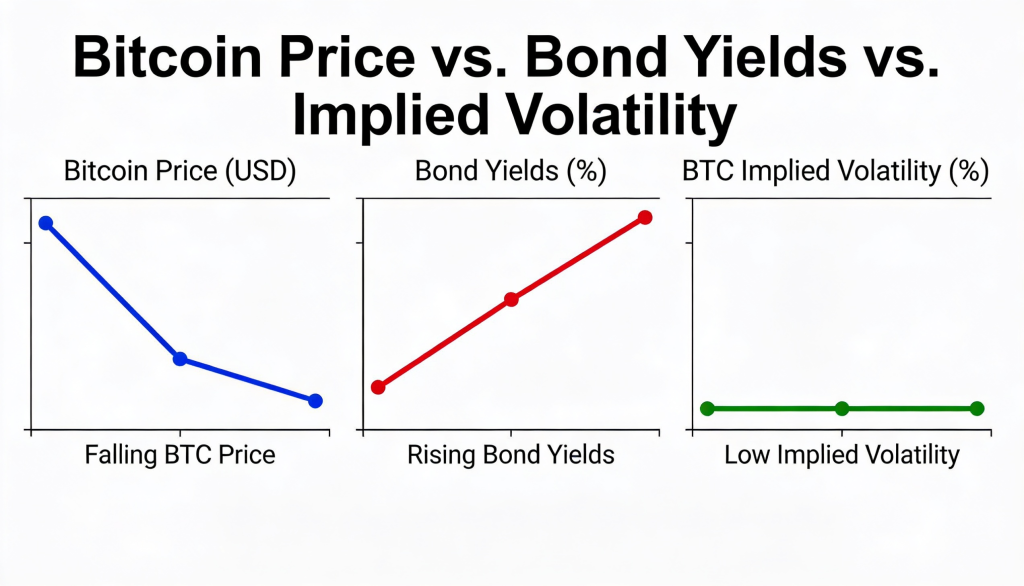

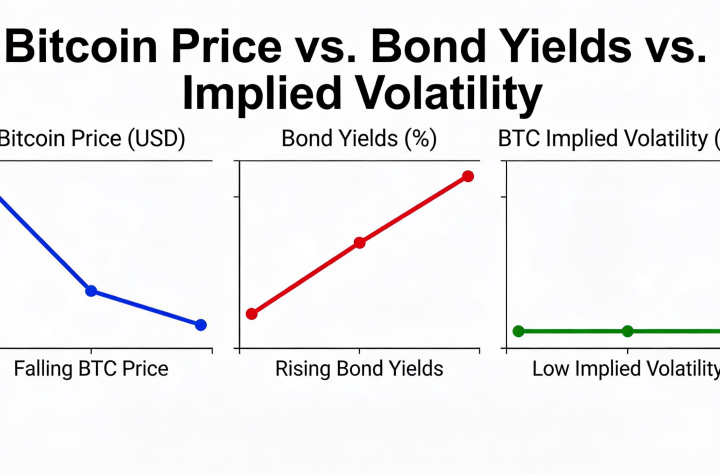

Bitcoin BTC $77,249.23 has declined in recent days, moving from around $82,000 to $77,000 since May 15, even as U.S. Treasury yields push higher. The combination of falling crypto prices and rising yields would typically signal heightened uncertainty—but Bitcoin’s options market is not reflecting that shift.

Instead, implied volatility, a forward-looking measure of expected price swings, has stayed relatively muted. That disconnect is drawing attention from derivatives traders who see potential for a repricing of risk.

The selloff—roughly 6%—has coincided with notable outflows from spot Bitcoin ETFs and firmer U.S. Treasury yields. At the same time, stress is also emerging in fixed income markets, with the MOVE index, which tracks implied volatility in U.S. Treasuries, rising sharply from 69% to 85%, highlighting growing turbulence in traditional markets.

Under normal conditions, such macro volatility would typically feed into crypto markets, pushing traders to buy options for protection and driving implied volatility higher. That has not happened so far.

Bitcoin’s 30-day annualized implied volatility index (BVIV) remains near 42%, according to TradingView data, only slightly above its year-to-date low of 40%. This suggests options markets are still pricing in relatively calm conditions despite recent price weakness.

That divergence is raising concerns that volatility risk may be underpriced. In other words, the options market could be failing to fully reflect the uncertainty building across macroeconomic indicators and cross-asset flows.

“In the options market, BTC IV is historically low: implieds have compressed to the high-30s/low-40s, printing new 2026 lows. That’s cheap vol in absolute terms,” said Jean-David Péquignot, Chief Commercial Officer at Deribit, the world’s largest crypto options exchange, which accounts for more than 70% of global crypto options activity.

According to Péquignot, the current environment makes long volatility strategies increasingly attractive. One such approach is the long straddle, where traders simultaneously buy a call and a put option at the same strike price and expiry.

This structure allows traders to profit from large price moves in either direction. If Bitcoin rallies, the call gains value; if it falls, the put provides upside. The strategy is designed for periods when traders expect significant movement but are uncertain about direction.

“BTC vol being this cheap while price is at a key breakout level can be a good setup for long vol / long straddle positioning ahead of a macro catalyst (next CPI print, Fed speech),” Péquignot added

More Stories

K33 says this Bitcoin bear market stands out, with “uniquely pessimistic” traders helping cap downside pressure.

According to Bitwise, Hyperliquid’s HYPE token stands out as one of crypto’s most undervalued opportunities.

Bitcoin slides $5K in a matter of days, with ETF outflows and derivatives pointing to deeper losses