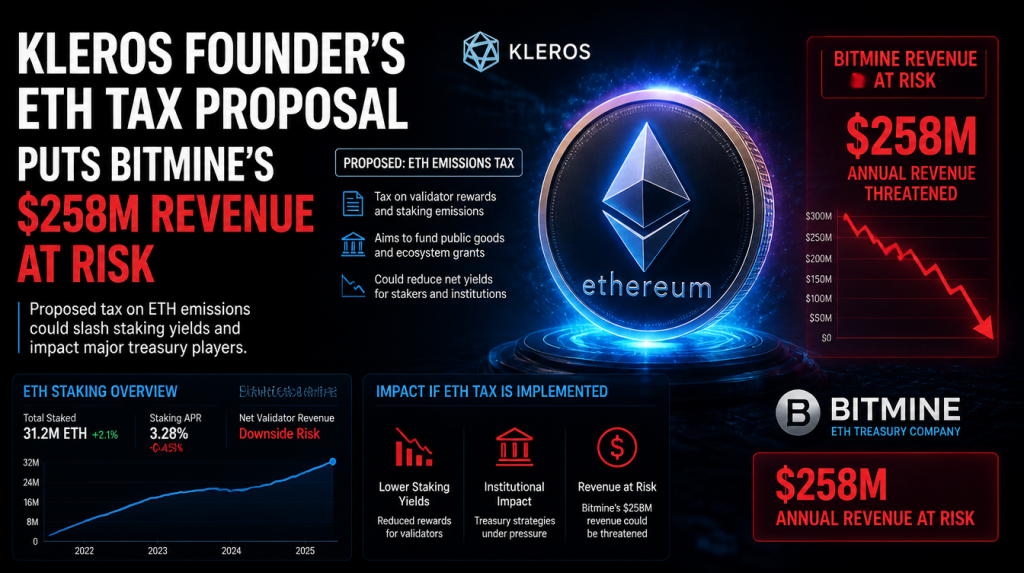

A proposal shared on the Ethereum Research forum by Kleros founder Clément Lesaege suggests allowing ETH validators to vote on redirecting up to 10% of staking rewards toward funding public goods. Should a majority of validators indicate any non-zero preference, the chosen rate would become compulsory across the network, applying even to validators that opted out.

For Bitmine (BMNR), which has staked 4.72 million ETH through its MAVAN platform and forecasts $258 million in annual net staking income, the potential financial impact ranges between $50 million and $100 million in lost yearly revenue.

This estimate is grounded in straightforward calculations, not speculation. It reflects the direct effect of an enforced reduction in yield on what is currently the largest ETH staking position held by a publicly traded company. While the idea remains at the discussion stage and has not yet been formalized as an Ethereum Improvement Proposal (EIP), its trajectory is worth close attention.

The ETH Validator Redirected Revenue Proposal

Lesaege’s concept, titled “Validator Redirected Revenue,” addresses what he views as a coordination gap. He argues that Ethereum’s shared infrastructure creates widespread value but lacks a built-in, protocol-level mechanism to fund its ongoing development.

To solve this, the proposal introduces a signaling mechanism at the consensus layer. Validators would specify a preferred redirection rate between 0% and 10% of their staking rewards. If more than half of the total staked ETH signals a rate above zero, a single unified rate would be determined and enforced network-wide.

Importantly, validators who vote for a 0% redirect would not be exempt if the majority threshold is reached. Instead, all participants would be subject to the same mandatory rate. The redirected funds would automatically flow into a smart contract, which would distribute them to designated beneficiaries such as Gitcoin, Octant, and security audit groups.

Lesaege emphasized that the proposal is still exploratory, noting that further feedback is needed before advancing toward a formal EIP. As of now, it has not been assigned an official proposal number.

A related concept, Validator Revenue Redistribution (VRR), introduced by Ethereum Foundation researcher Devansh Mehta at EthCC, outlines the technical framework. As Mehta explained, once 51% of validators opt in, the rule applies universally, requiring all stakers to contribute a portion of their rewards.

Bitmine’s MAVAN Platform and Revenue Exposure

According to Bitmine’s May 8-K filing, the firm has staked 4,718,677 ETH via its MAVAN platform—representing 87% of its total 5.42 million ETH holdings and approximately 4.49% of the total ETH supply. At the time, the 7-day annualized yield stood at 2.73%, slightly below the CESR benchmark range of 2.81% to 2.84%. At full scale, Bitmine projects $296 million in gross staking rewards and $258 million in net annual staking revenue.

The financial implications of a protocol-level redirect are relatively straightforward. A 1 percentage point decline in annual yield on 4.72 million ETH equates to roughly $94 million in lost gross rewards, assuming an ETH price near $2,000.

Under the current proposal, a 10% redirect applied to a 2.73% yield translates to a 0.27 percentage point reduction, or about $25 million annually diverted away from Bitmine’s validators. While significant, this impact alone would not be catastrophic.

However, the broader projected exposure of $50 million to $100 million reflects more complex scenarios. These include potential secondary pressures such as declining validator incentives, institutional capital rotating toward restaking or Layer-2 yield opportunities, and fluctuations in ETH price—all of which could further compress effective yields across Bitmine’s staked assets.

Staking revenue is central to Bitmine’s business model, accounting for over 93% of its quarterly revenue in Q2 FY2026. The company also introduced a $0.01 annual dividend in January 2026, funded directly through staking income—making it the first large-cap crypto firm to do so.

Any meaningful reduction in yield would place this dividend under strain, in ways that operational adjustments alone cannot resolve. Unlike typical business costs, an ETH validator tax would represent a protocol-level change, directly reducing returns from the underlying asset rather than something the company can mitigate through strategy or execution.

More Stories

Taiko Pauses Ethereum Layer-2 Network After Bridge Exploit Triggers Token Crash

Bitcoin Reclaims $65K as Markets Bounce; Strategy Boosts Cash and Bitcoin Holdings

Bitcoin Holds Near $64K as US–Iran Talks Advance While Crypto Markets Lag the Risk Rally