Bitcoin’s volatility continues to ease, mirroring trends in the S&P 500, and casting doubt on a potential year-end rally, analysts say.

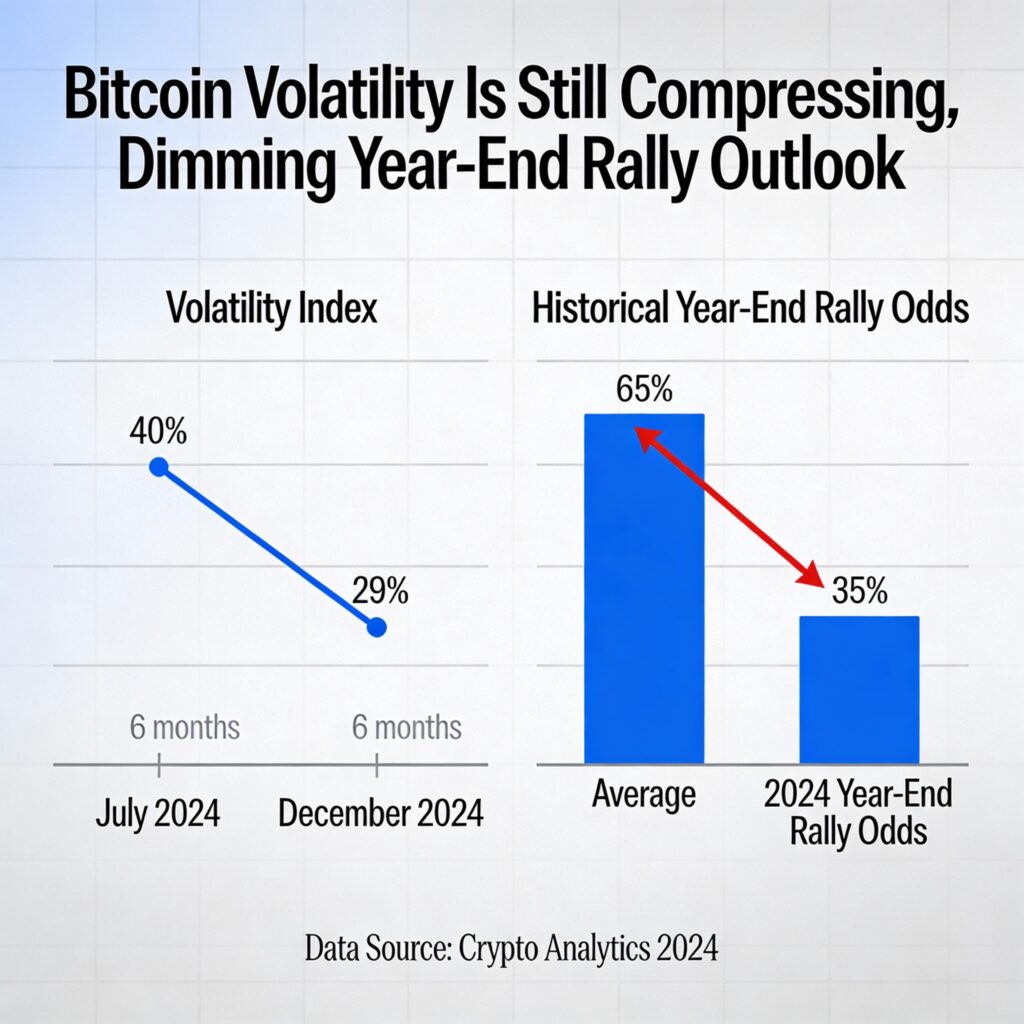

BTC’s 30-day annualized implied volatility, tracked by Volmex’s BVIV index, has dropped to 49%, nearly reversing a spike from 46% to 65% over the 10 days through Nov. 21, according to TradingView. Implied volatility, derived from options pricing, reflects expected price swings over a set period, and the decline signals reduced market turbulence over the coming month.

The S&P 500’s VIX index has also retreated, falling from 28% on Nov. 20 to 17%.

Matrixport highlighted that this volatility compression lowers the likelihood of a significant year-end bitcoin rally. “Implied volatility continues to compress, and with it, the probability of a meaningful upside breakout into year-end,” the firm said in a Wednesday market update. “The FOMC meeting is the last major catalyst, but volatility is expected to drift lower afterward.”

Historically, bitcoin’s price has moved in tandem with volatility, though the correlation has shifted toward negative since November 2024. On Wall Street, similar periods of low implied volatility often precede bullish resets, illustrating the mixed signals facing bitcoin as the year closes.

More Stories

Bitcoin holds near $68,300 while gold tumbles for a ninth session and Asian stocks fall

Resolv stablecoin drops 70% as exploiter siphons $25 million worth of ETH

Equities catch up to bitcoin’s drop toward $60,000 amid a surge in bond yields.