Cantor: Coinbase Is More Than an Exchange—It’s Critical Crypto Infrastructure

Cantor Fitzgerald has launched coverage of Coinbase (COIN) with an overweight rating and a price target of $245, arguing that the exchange’s long-term potential is significantly undervalued by the market. The report pushed Coinbase stock over 5% higher in early trading.

The firm emphasized that Coinbase’s Layer 2 network, Base, and its strategic partnership with Circle around stablecoins are underappreciated assets that go well beyond trading revenue.

“Base’s rapid adoption is generating strong transactional volume and creating a flywheel effect for Coinbase’s ecosystem,” wrote analysts Brett Knoblauch and Thomas Shinske. “Meanwhile, its role in stablecoin infrastructure could position it at the center of future global payment rails.”

Cantor noted that Coinbase is currently trading 32% below its historical multiples, and sees upside as the market begins to recognize the company’s broader role in crypto infrastructure.

Rather than viewing Coinbase as just a cyclical play tied to crypto prices, the report suggests it should be seen as a core building block of Web3 and decentralized finance.

“As visibility into revenue from Base and stablecoin activity improves, we expect a rerating of the stock,” the analysts wrote.

More Stories

Bitcoin drops under $71,000 while stocks end the day near session lows as expectations for a 2026 Fed rate cut dim further.

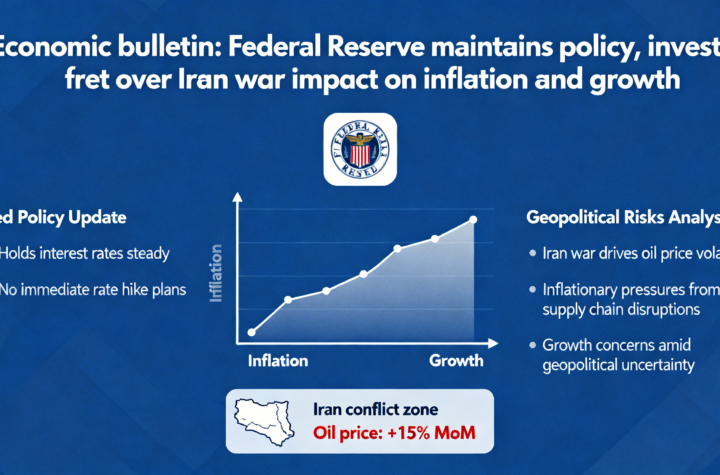

Fed pauses rate changes as the Iran conflict clouds the economic outlook and fuels inflation fears.

Cheap money is now behind us as ongoing conflict with Iran locks in a higher baseline for inflation.