Bitcoin Volatility Outpaces S&P 500, Signaling Potential Pair Trade

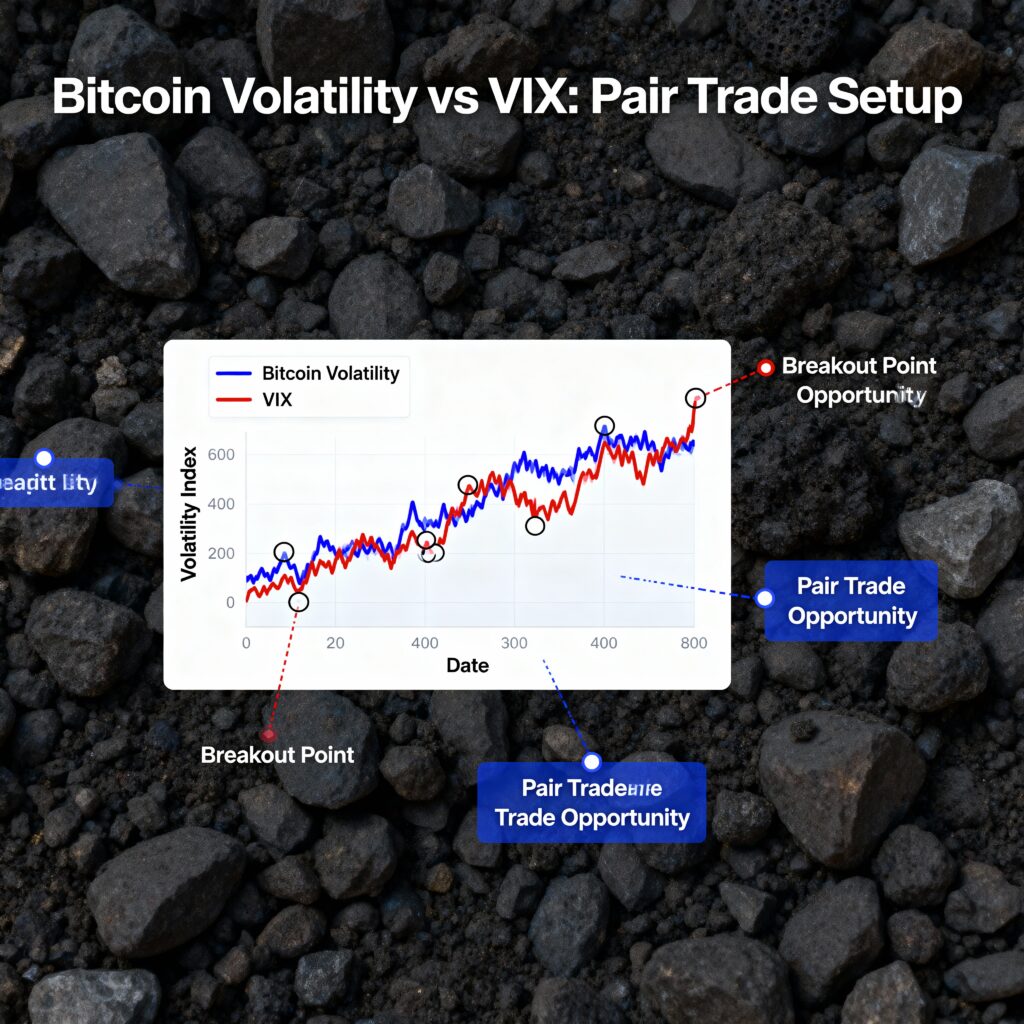

The spread between Bitcoin (BTC) and S&P 500 implied volatility indices is widening again, suggesting that BTC may experience greater volatility than equities in the near term.

The gauge tracks the difference between Volmex’s BVIV—the 30-day implied volatility index for BTC—and the VIX, the S&P 500 volatility benchmark. Implied volatility reflects demand for options and hedging instruments, and a widening spread signals that crypto markets are pricing in stronger price swings relative to equities.

“When the BVIV–VIX spread widens, it usually indicates that markets expect higher crypto volatility than equity volatility,” said Cole Kennelly, Founder of Volmex. “Crypto options respond faster to liquidity shifts and macro catalysts, so implied volatility often moves ahead of traditional markets.”

The spread recently broke out of a months-long range of 20.000–32.000 and surpassed the downtrend from March 2024, pointing to higher near-term BTC volatility.

This dynamic could attract pair traders who take opposing volatility positions in BTC and equities. Kennelly noted, “Traders often view a significant BVIV–VIX widening as a relative value opportunity, expressed via multi-legged cross-asset volatility trades rather than simple directional bets.”

Volatility trading, which involves wagering on price swings rather than market direction, is capital-intensive, risky, and requires constant monitoring, making it primarily suitable for institutional investors.

More Stories

Bitcoin holds near $68,300 while gold tumbles for a ninth session and Asian stocks fall

Resolv stablecoin drops 70% as exploiter siphons $25 million worth of ETH

Equities catch up to bitcoin’s drop toward $60,000 amid a surge in bond yields.