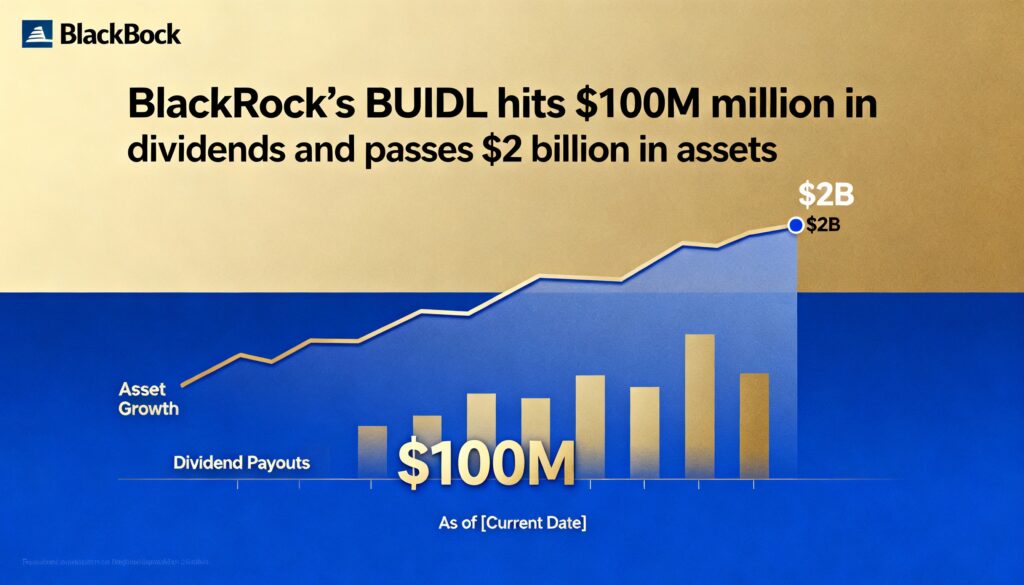

BlackRock’s tokenized money market fund BUIDL has paid out about $100 million in dividends since its launch in March 2024, marking a key milestone for blockchain-based financial products operating at institutional scale. The figures were confirmed by Securitize, which serves as the fund’s transfer agent and administrator.

The fund invests in short-term U.S. Treasuries, repurchase agreements and cash-equivalent instruments, and has grown to more than $2 billion in assets. That growth makes BUIDL one of the largest tokenized cash products in the market and the first tokenized Treasury-backed fund to surpass $100 million in cumulative dividend distributions.

Structured as a regulated money-market-style vehicle, BUIDL differs from stablecoins by offering tokenized fund shares rather than a pegged digital asset. Those shares settle on public blockchains and allow qualified institutional investors to earn and receive yield directly onchain. Initially launched on Ethereum, the fund has since expanded to multiple networks as demand for onchain dollar-denominated yield products has increased.

BUIDL’s role has extended beyond yield generation. The tokens are now embedded in crypto market infrastructure, serving as collateral in trading and financing arrangements and as backing for stablecoins such as Ethena’s USDtb. This integration highlights how tokenized funds are increasingly being used as building blocks within decentralized financial markets.

Tokenized money market funds have expanded rapidly over the past year as institutions look for regulated alternatives to stablecoins that provide yield on dollar exposure. At the same time, regulators and policymakers have raised concerns around settlement finality, liquidity assumptions and how tokenized securities may perform during periods of market stress.

BUIDL’s adoption underscores its position at the crossroads of traditional short-term interest-rate markets and the broader effort to move collateral, settlement and yield strategies onto blockchains.

More Stories

Bitcoin holds near $68,300 while gold tumbles for a ninth session and Asian stocks fall

Resolv stablecoin drops 70% as exploiter siphons $25 million worth of ETH

Equities catch up to bitcoin’s drop toward $60,000 amid a surge in bond yields.