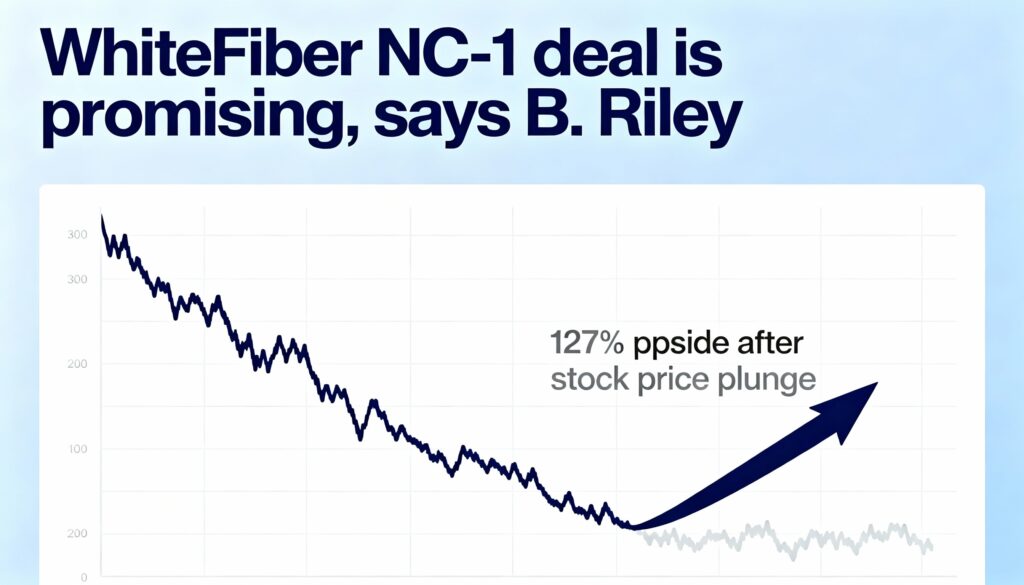

WhiteFiber’s first long-term colocation deal at its NC-1 campus signals early validation of the company’s retrofit-led strategy, B. Riley said in a report Tuesday.

The agreement with Nscale Global demonstrates management’s ability to execute while remaining on its original deployment schedule, according to analysts Nick Giles and Fedor Shabalin. They said reaffirming the timeline underscores both operational discipline and the benefits of WhiteFiber’s retrofit model.

B. Riley reiterated its buy rating on WhiteFiber (WYFI) but cut its price target to $40 from $44, citing more conservative assumptions for the Cloud Services segment. Even after the reduction, the target implies roughly 127% upside from the stock’s latest close of $17.62. Shares remain more than 50% below their record high set about two months ago.

The analysts also noted that WhiteFiber is in advanced talks with lenders over a construction financing facility expected to close in early 2026. The facility could include an accordion feature and credit enhancements, potentially lowering the company’s cost of capital.

From a valuation perspective, B. Riley said WhiteFiber is trading at around 11 times its 2026 EV/EBITDA estimate and about 8 times EV/EBITDA based on its fourth-quarter 2026 adjusted EBITDA run rate, which the firm views as a meaningful discount to peers trading in the mid- to high-teens.

More Stories

Strategy Launches Bitcoin Monetization Plan as Saylor Unveils Buybacks and Dividend Boost

Bitcoin Stalls Below $60K as Crypto Faces Crucial Week Ahead

Bitcoin Enters Technical No Man’s Land as Key Support Levels Drift Lower