Strategy Becomes First Bitcoin Treasury Firm Rated by S&P Global

S&P Global has assigned a B- credit rating to Michael Saylor’s Strategy (MSTR), marking the first time a major credit agency has formally rated a bitcoin-focused treasury company.

The B- rating, however, lands Strategy deep in speculative territory, reflecting S&P’s view that the company’s bitcoin-centric model carries high financial risk despite its strong balance sheet and capital markets access.

According to S&P, a “B” rating indicates speculative credit quality with elevated default risk. A B- sits just above the “CCC” range, signaling heightened vulnerability to adverse market conditions.

Strategy, once an enterprise software firm, has reinvented itself as a publicly traded bitcoin holding vehicle. The company routinely converts excess cash into bitcoin and funds much of its activity through convertible debt, preferred stock, and equity issuance.

Executive Chairman Michael Saylor called the rating “a milestone moment,” noting that Strategy is the first-ever bitcoin treasury company recognized by a major credit agency. David Bailey, CEO of KindlyMD (NAKA), said the move highlights “growing institutional demand for bitcoin balance sheet exposure.”

S&P’s Assessment

As of mid-2025, Strategy held approximately $70 billion in bitcoin against $15 billion in outstanding convertible debt and preferred equity. Despite the asset strength, S&P cited limited cash reserves and weak operating income, with the firm posting a $37 million operating cash outflow in the first half of 2025.

The agency also flagged a currency mismatch: nearly all of Strategy’s assets are denominated in bitcoin, while its debts and dividend payments are in U.S. dollars. That mismatch could pressure the firm to sell BTC during market downturns to meet obligations.

S&P further noted the company’s negative total adjusted capital, an accounting result of excluding bitcoin from equity due to its volatility and lack of correlation to traditional assets.

Another concern is the $640 million in annual preferred stock dividends. Although Strategy can defer these payments, doing so would trigger governance provisions such as preferred shareholders gaining board representation. The firm has said it intends to fund dividends through new equity issuance rather than bitcoin sales.

Outlook Remains Stable

Despite the risks, S&P assigned a stable outlook, citing the company’s proven access to capital markets and manageable debt maturities, with no major repayments due until 2028.

An upgrade is considered unlikely in the near term unless Strategy meaningfully strengthens its dollar liquidity and reduces reliance on convertible debt. A downgrade could occur if market access tightens or if bitcoin’s price weakens significantly.

For now, S&P’s message is clear: Strategy’s financial health is inseparable from bitcoin’s price performance — a dynamic that defines both its strength and its risk.

Shares of MSTR rose nearly 3% on Monday, tracking bitcoin’s rally to about $115,500.

More Stories

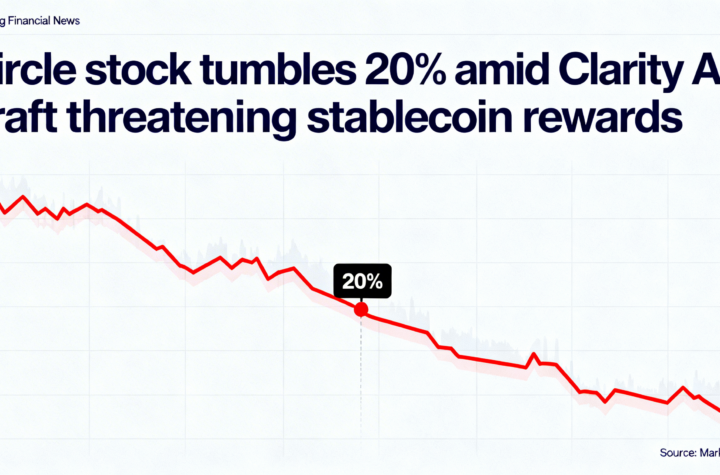

Circle stock drops 20% after new Clarity Act draft threatens stablecoin yield incentives.

Bitcoin falls under $70K, with Circle’s 16% slide leading declines in crypto stocks.

Has Bitcoin already bottomed near $60,000? Here’s why it might have.