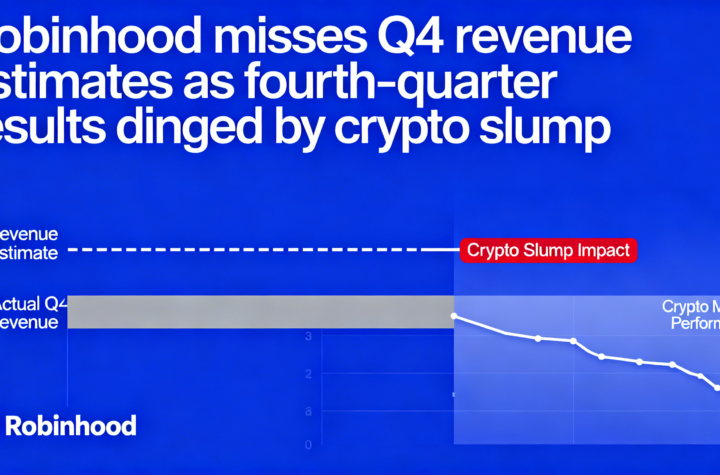

Shares of Robinhood fell 10% in early Wednesday trading after the company reported fourth-quarter revenue that missed Wall Street expectations, as a slowdown in cryptocurrency trading weighed on overall performance.

The brokerage posted earnings per share of $0.66, ahead of the $0.63 consensus estimate. Revenue, however, came in at $1.28 billion, below the $1.33 billion analysts had forecast.

Crypto activity was a key drag on the quarter. Revenue from digital asset trading declined 38% year over year to $221 million, contributing to transaction revenue of $776 million that also fell short of expectations. The weakness followed a late-year slump in digital asset markets.

Net interest revenue totaled $411 million, missing estimates as softer securities lending activity and lower yields pressured results.

In response, several sell-side firms lowered their price targets. JPMorgan reduced its target to $113 from $130 and maintained a Neutral rating, citing the softer quarter and tougher comparisons in 2025 that could make 2026 growth harder to achieve. Even at the revised level, the target implies more than 50% upside from the recent share price near $76.50.

JPMorgan analysts, led by Kenneth Worthington, noted that although January trading volumes improved year over year, growth across key operating metrics appears to be moderating. The bank trimmed its revenue forecasts accordingly.

Compass Point took a more optimistic stance despite lowering its price target to $127 from $170 and reiterating a Buy rating. Analyst Ed Engel pointed to solid January key performance indicators across business lines, including crypto volumes that came in better than feared following the weak fourth quarter.

Still, Engel acknowledged a 9% EBITDA miss, driven by lower securities lending revenue and declining take rates in both crypto and options trading. He highlighted management’s guidance for 18% operating expense growth in 2026 as a notable development, suggesting the increased spending will support expansion into crypto, DeFi, and prediction markets.

While those investments could drive growth in the second half of 2026, Engel cautioned that investors may temper near-term EBITDA expectations. He also cited potential longer-term catalysts, including internalization of prediction markets and prospective IPOs from companies such as SpaceX, Anthropic, and OpenAI.

Finally, Engel noted that Robinhood’s crypto take rate fell three basis points sequentially in the fourth quarter and has declined an additional five basis points so far in 2026, reflecting a growing mix of higher-volume traders on the platform.

More Stories

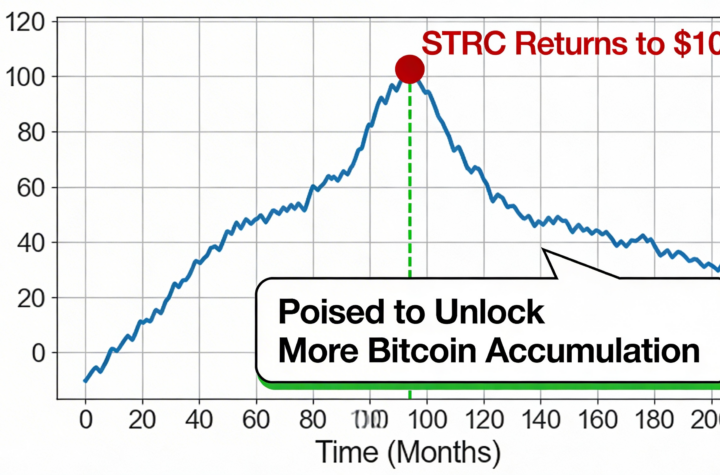

STRC returns to the $100 mark, positioning Strategy for further Bitcoin purchases.

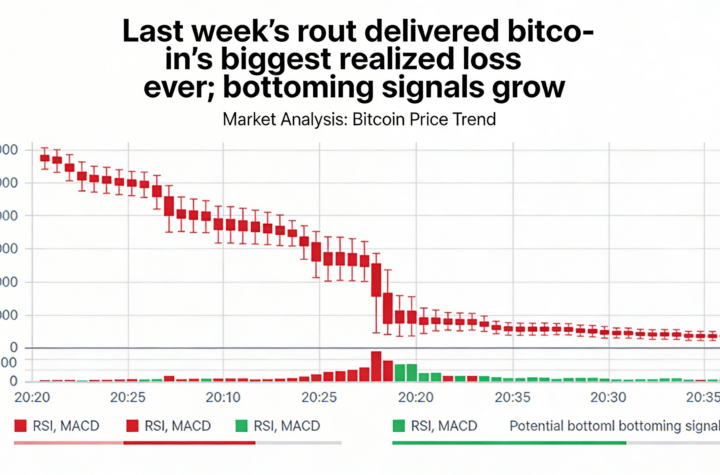

Bitcoin logged its biggest realized loss ever during last week’s rout, with bottoming signals now building.

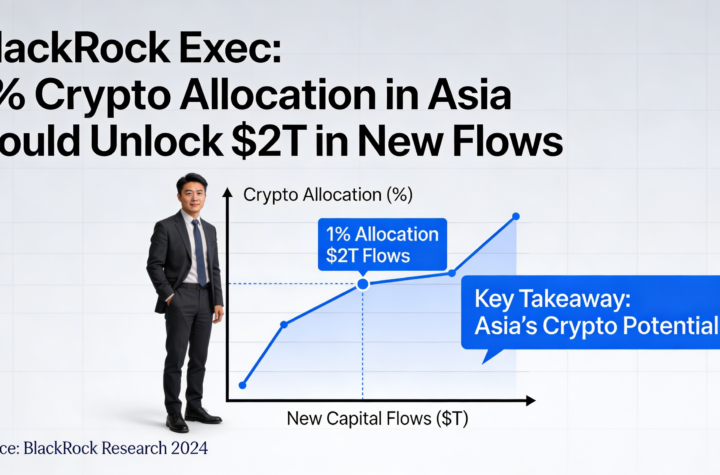

A 1% shift into crypto by Asian investors could generate $2 trillion in new capital, says a BlackRock exec.