After a prolonged period of market calm, Bitcoin’s implied volatility (IV) is beginning to stir—potentially setting the stage for a major price move.

The Deribit Volatility Index (DVOL), which reflects the 30-day implied volatility of bitcoin options, jumped from 33 to 37 on Monday. This marks the highest reading in several weeks and follows a sharp rebound from last week’s multi-year low of 26%, a level not seen since August 2023, when BTC traded near $30,000 before a breakout rally.

Implied volatility gauges expectations for future price swings based on option premiums. Rising IV suggests traders are anticipating larger moves ahead, especially when paired with expanding spot market activity.

Over the weekend, Bitcoin surged from $116,000 to $122,000, signaling how rapidly momentum can return as volatility picks up. Historically, these quiet periods often precede explosive price action.

Despite August typically being a slower month for trading, the IV spike suggests growing anticipation of a directional shift. According to Checkonchain, the recent rally was spot-led rather than leverage-driven, reflecting stronger market structure. At the same time, declining open interest throughout August indicates that if leverage reenters the market, it could significantly amplify price moves.

With Bitcoin trading just shy of its all-time highs, traders appear to be repositioning in expectation of heightened volatility—potentially the “calm before the storm.”

More Stories

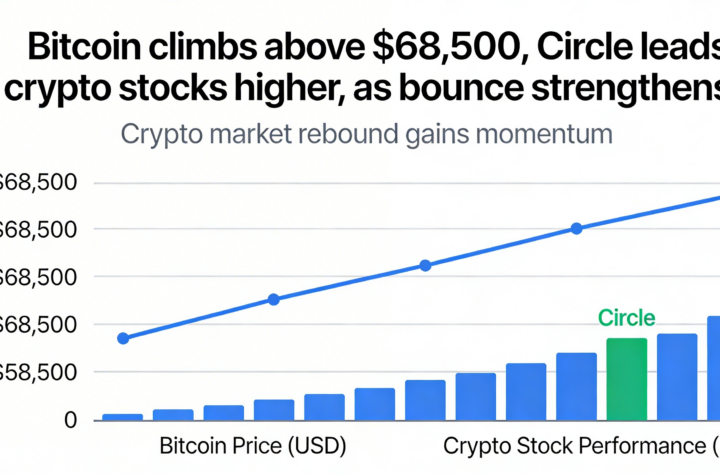

A firmer bounce lifts Bitcoin above $68,500, with Circle driving upside momentum across crypto stocks

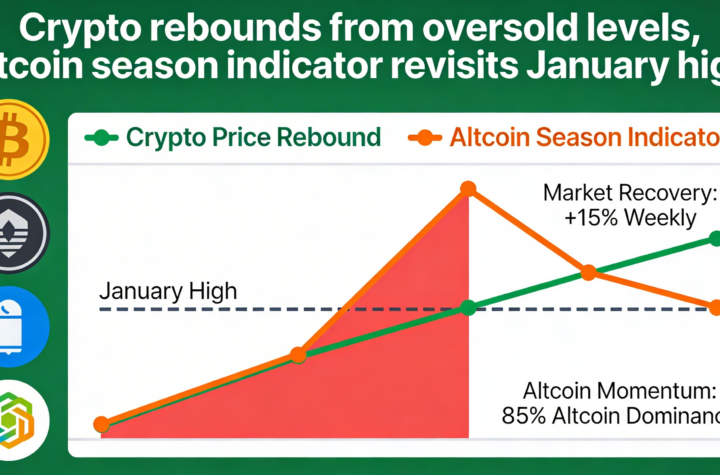

Crypto stages a rebound from technical lows while the altcoin season indicator revisits levels last seen in January.

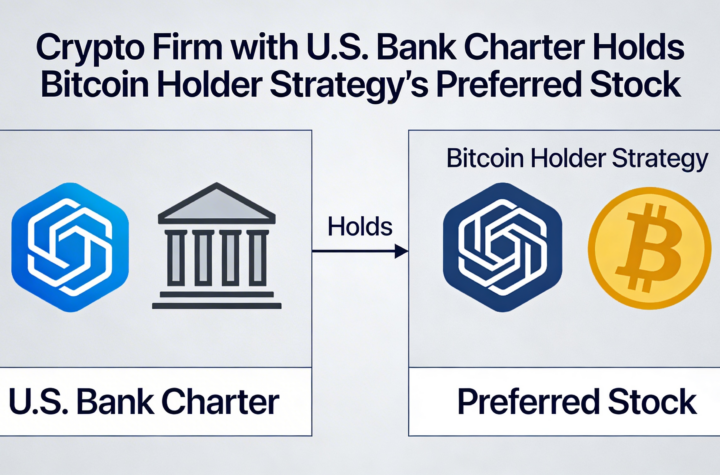

The U.S.-chartered crypto firm has taken a position in preferred stock from bitcoin treasury company Strategy.