Bitcoin Bulls in the Driver’s Seat No Matter How Jobs Data Lands

Bitcoin is back above $84K and holding steady — and with the March U.S. jobs report set to drop, bulls may be looking at a no-lose situation.

After a volatile week marked by President Trump’s surprise 10% tariffs on imports from 180 countries, investors are shifting their focus to macro data and rate cut probabilities. The market’s mood? Surprisingly optimistic.

Heads or Tails — Bulls Win Either Way

Whether the jobs report comes in hot or cold, the current setup favors upside for BTC:

- Strong jobs data? Traders may shrug it off, viewing it as outdated in light of Trump’s aggressive trade stance and the potential economic drag.

- Weak numbers? That’ll likely fuel rate cut bets and pump risk assets, crypto included.

Either way, bitcoin is well-positioned to rally.

Market Signals: No Panic, Just Patience

Despite dipping below $82K on Thursday, BTC bounced quickly and remains far above its March low of $77,000. That suggests seller exhaustion, not panic.

Volmex’s Bitcoin IV index shows 65% annualized volatility, which implies a 3.4% move over the next 24 hours — nothing wild, just enough to keep things interesting.

All Eyes on Payrolls

The nonfarm payrolls report lands at 12:30 UTC. Economists expect 130,000 new jobs, a step down from February’s 151,000, with unemployment ticking up to 4.2%.

That’s exactly the kind of slowdown the Fed might need to justify cutting rates — and bitcoin could thrive in the aftermath.

Bottom Line

In a market where expectations matter as much as reality, BTC bulls may have already won the coin toss.

More Stories

Bitcoin drops under $71,000 while stocks end the day near session lows as expectations for a 2026 Fed rate cut dim further.

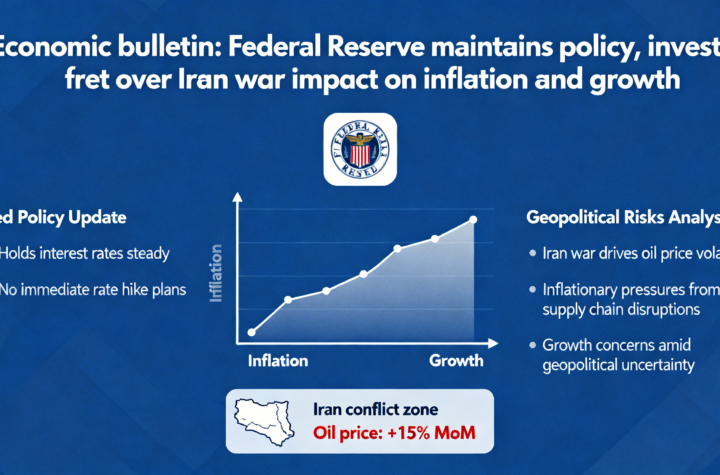

Fed pauses rate changes as the Iran conflict clouds the economic outlook and fuels inflation fears.

Cheap money is now behind us as ongoing conflict with Iran locks in a higher baseline for inflation.